How to Sell a House in Pre Foreclosure in San Antonio

Facing missed payments can be overwhelming, but if your home is in pre foreclosure you still have options. Pre foreclosure is the period after you fall behind on your mortgage but before the lender has formally repossessed the property. During this window you can catch up on your loan or sell the home to avoid a full foreclosure. This guide explains the process, the laws in Texas and how to make the most of your situation.

Hi, I’m Daniel Cabrera, founder of Sell My House Fast SA TX, and over my 16+ years in San Antonio real estate, I’ve helped hundreds of homeowners sell house in pre-foreclosure situations, often closing in less than a week and allowing them to move forward without the burden of foreclosure on their credit. My background in construction, finance, and investment banking gives me a unique perspective on navigating these complex situations with speed and compassion.

Quick Answer: Can You Sell a House in Pre-Foreclosure?

- Yes, you can legally sell your home at any point before the foreclosure auction date (usually the first Tuesday of the month in Texas)

- You keep any equity after paying off the mortgage, late fees, and closing costs

- Selling protects your credit far better than a foreclosure (which stays on your report for 7 years)

- No repairs needed when you sell as-is to a cash buyer like Sell My House Fast SA TX

- Fast timeline possible with same-day offers and closings in as little as one week

What Is Pre Foreclosure?

Pre foreclosure means your mortgage is in default but the lender has not yet started the formal foreclosure process. It is the initial stage of foreclosure: you are behind on payments but still have time to work with your lender or sell the property. In Texas and many other states, homeowners receive a Notice of Default when payments are significantly overdue, but they can still resolve the debt or sell the home. Pre foreclosure is distinct from foreclosure – foreclosure begins when the lender files a lawsuit or trustee’s sale to take possession.

Why Pre Foreclosure Occurs

Mortgage delinquency can happen for various reasons: job loss, medical bills or unexpected expenses. When you miss one or more payments, lenders typically grant a grace period, but repeated non payment triggers a default notice. At this point the lender may issue a Notice of Default and start contacting you. That notice marks the beginning of pre foreclosure. If you ignore it, the loan may accelerate to full foreclosure.

Texas Timeline and Legal Requirements

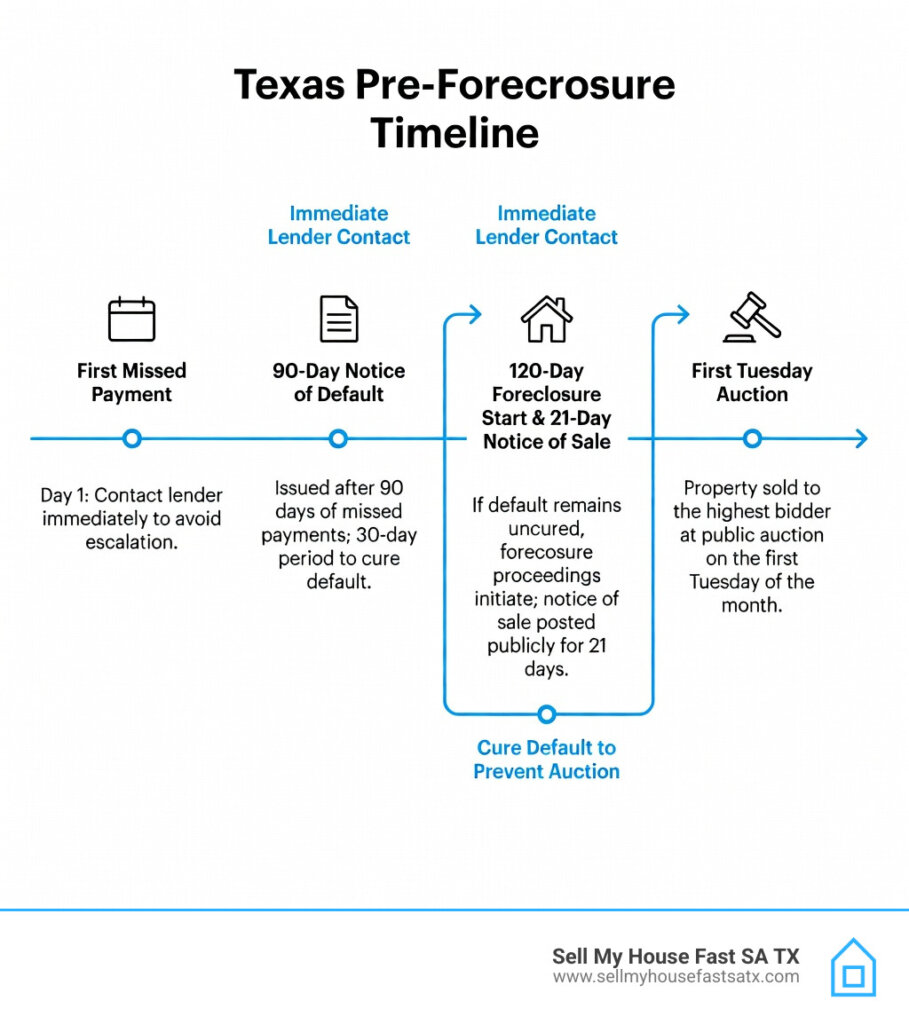

Texas has strict timelines for foreclosure. Federal regulations state that lenders cannot begin foreclosure until the loan is more than 120 days delinquent. In a non judicial foreclosure, which is the most common method in Texas, homeowners receive a Notice of Default and usually have 20 days to reinstate the loan by paying the past due amount. After that, if they cannot reinstate, the lender must send a Notice of Sale at least 21 days before the auction. These notices must also be posted publicly at the courthouse. Knowing these deadlines is critical when planning to sell house in pre foreclosure in San Antonio because the sale needs to close before the auction date.

In Texas, foreclosure auctions typically occur on the first Tuesday of each month from 10:00 a.m. to 4:00 p.m.. The lender sets a minimum bid based on the outstanding loan balance and fees. If no one bids above that amount, the property becomes Real Estate Owned (REO) by the lender. Buyers and sellers should understand this schedule because it affects your ability to sell your house before foreclosure.

Selling a Home in Pre Foreclosure

Selling the property before the foreclosure sale is one of the most effective ways to avoid foreclosure and save your credit. Many people search for selling a home in preforeclosure or sell house in preforeclosure because they want to clear the debt and move on. Here are the key steps:

- Assess the Property and Market. Get a realistic valuation of your home based on current market conditions. Consider any fire or water damage and decide whether repairs are worth the cost. Pricing the home correctly is crucial.

- Discuss Options with Your Lender. Ask about reinstatement, forbearance or a repayment plan. Federal law requires lenders to wait until the loan is 120 days delinquent before starting foreclosure, so use this period to negotiate.

- Market the Home Aggressively. Use multiple channels – local listings, online platforms and signage – to reach buyers quickly. Highlight the strengths of the property and explain its pre foreclosure status honestly.

- Negotiate and Close Quickly. Time is limited, so be prepared to negotiate both with potential buyers and with the lender to agree on sale terms. We recommend working with cash buyers as they are experienced in distressed sales.

During pre foreclosure you can still work with a real estate agent or sell directly to investors. Agents knowledgeable in foreclosure transactions can help with pricing and marketing, but they charge a commission and may not control the timeline. Local investors, like Sell My House Fast SA TX, often purchase properties for cash. Cash offers can close quickly and often cover closing costs, which helps if you need to sell your house fast before foreclosure or sell house in pre-foreclosure.

Can You Sell a House in Pre-Foreclosure?

Yes, you can sell house in pre foreclosure in San Antonio until the foreclosure auction. Once the auction takes place the property is sold to the highest bidder or goes back to the lender. If you are late in the process you may need to pursue a short sale, where the lender agrees to accept less than the full mortgage balance. Short sales require lender approval and can take time, but they still prevent a completed foreclosure. Law firm resources explain that a short sale can minimize the impact on your credit. Companies specializing in pre foreclosure short sales can guide you through the process.

Other Ways to Avoid Foreclosure

Selling is not the only option. Here are other methods to avoid foreclosure in San Antonio:

- Loan Forbearance or Repayment Plan. A forbearance agreement temporarily reduces or suspends payments, giving you time to get back on track. After the forbearance period you repay the missed amounts via higher payments or an extended loan term.

- Loan Modification. A permanent change to your loan terms can lower interest rates or extend the repayment period. This reduces monthly payments, but not all lenders approve modifications.

- Short Sale. Sell the property for less than what you owe, with lender consent. Short sales can affect your credit but are less damaging than a foreclosure and may include debt forgiveness.

- Deed in Lieu of Foreclosure. Transfer ownership back to the lender to avoid foreclosure and deficiency judgments. You should consult a legal professional to understand the implications.

- Bankruptcy. Filing Chapter 7 or Chapter 13 bankruptcy can halt foreclosure temporarily and allow for debt restructuring. This is a serious step and requires professional advice.

These options can help homeowners dealing with house in preforeclosure but each has tradeoffs. Discuss them with a housing counselor or attorney.

Local Investors and Cash Buyers

Working with a local investor can be ideal when you need to sell house fast due to pre foreclosure. These buyers typically:

- Provide quick cash offers for homes in any condition.

- Purchase the property as is, so you do not have to invest in repairs.

- Cover closing costs and avoid agent commissions.

- Close within days, which is essential when you are racing against a foreclosure auction.

When choosing a buyer, verify their track record, request proof of funds and read reviews. A reliable firm will explain the process and not pressure you. In San Antonio you will find many companies advertising to buy your house, so choose carefully.

We have over 16+ years in San Antonio real estate, we’ve helped hundreds of homeowners sell house in pre-foreclosure situations, often closing in less than a week and allowing them to move forward without the burden of foreclosure on their credit.

Don’t just take our word for it, see what our satisfied clients have to say!

“Brett Favre here with Sell My House Fast San Antonio – where every second counts. They offer precision, expertise and a strategy designed to San Antonio’s unique market. They guarantee a fair and fast no-obligation cash offer without delays. Step off the sidelines and into the game with Sell My House Fast San Antonio Texas for a swift sale. Give them a call at 210-951-0143“

– Brett Favre

We are also featured in:

Frequently Asked Questions About Pre Foreclosure

Can I sell my house in pre foreclosure if it is fire damaged?

Yes. You can sell a house in pre foreclosure in any condition, including properties with fire or water damage. Investors often purchase homes as is and close quickly. Selling to a cash buyer allows you to avoid repair costs and move on, even if the home needs work. This option is popular among owners looking to sell their house fast due to pre-foreclosure or to sell house in foreclosure because it delivers a fast solution and prevents the foreclosure from being finalized.

What happens to my credit if I sell my house during pre foreclosure?

Selling before the auction usually has a smaller impact on your credit than letting the foreclosure proceed. A short sale or pre foreclosure sale may still lower your credit score, but it is far less damaging than a completed foreclosure. If you can settle the loan in full by selling, you avoid a deficiency judgment and start rebuilding your credit sooner. This is why many owners look for ways to sell their house before foreclosure in San Antonio.

How long do I have to sell my house before foreclosure in Texas?

The window between default and foreclosure is typically around six months. Federal rules say lenders cannot start foreclosure until the loan is at least 120 days past due. After that, Texas law requires the lender to send a Notice of Sale at least 21 days before the auction. Because auctions in Texas are held on the first Tuesday of each month, you should list or market the property immediately if you plan to sell house in pre foreclosure in San Antonio.

Can I buy a house in pre foreclosure directly from the owner?

Yes. You can contact homeowners in default and make an offer. Research the property’s liens, repair costs and the foreclosure timeline. If the seller needs lender approval for a short sale, be prepared for extra paperwork. Ethically, treat sellers with respect and acknowledge that they may be under stress.

Do I need a real estate agent to sell my house in pre foreclosure?

Not necessarily. Real estate agents can help with pricing and marketing, but they charge commissions and may not control the sale timeline. Many homeowners choose to work directly with San Antonio investors like Sell My Houst Fast SA TX. These buyers close faster, cover closing costs and purchase properties as is. Decide whether you value maximum sale price or speed and choose the option that best fits your situation.

Conclusion and Next Steps

Pre foreclosure can feel daunting, but there is a path forward. You can sell your house before foreclosure in San Antonio or negotiate alternatives with your lender. Understanding timelines, knowing your rights and exploring options such as loan modifications or short sales will help you make informed decisions. If you prefer a fast sale, Request a Free, No-Obligation Cash Offer Today by fill the form below or call us at (210)951-0143.

You’re just one step from getting a FREE cash offer for your home!

Get a FREE cash offer on your San Antonio property today and move on from the headache of a stressful house.